January 2, 2025

5 Predictions Defining 2025

Tim Urbanowicz, CFA

Chief Investment Strategist

Innovator Capital Management

New year, new beginnings. Outside of the gym becoming overly crowded for a few weeks, before New Year’s resolutions begin to fade, it’s one of my favorite times of the year. I’m all about personal and professional goal-setting, attempting to start new good habits, and break bad ones. And on Wall Street, it’s prediction season. What’s not to love?

Sticking with the nature of the season, in the first edition of Dialed In for 2025, we are going to outline five predictions across financial markets throughout the year. To preface, when looking at predictions, I personally find great value in the thought process, and very little value in the prediction itself. The thought process highlights certain risks and opportunities, so let’s focus on that. So here are my top 5 for ‘25!

10-Year Treasury Yields Could Rise

Several strategists had dubbed 2024 the "year of the bond," banking on half a dozen Fed rate cuts. It’s been anything but that. Fewer Fed cuts, a strong economic outlook, and inflation fears have sent the 10-year yield roughly 70bps higher than where it closed out 2023, and once again, bond investors are left holding the bag.

I believe 2025 will tell a similar story. Investors are pricing in three or more 25bps cuts in the new year. In my view, that’s too many. With pro-growth policies coming from the Trump administration, a sticky base of 2.8% on Core CPI, and immigration restrictions that could take supply out of the labor market resulting in upward pressure on wage growth, I struggle to see this playing out as anticipated. It may sound crazy, but I wouldn’t even be shocked if we saw a rate hike before the year was over.

Even if market expectations are right and the Fed funds rate hits 3.75% in 2025, yield curve normalization (i.e., an upward sloping yield curve) could still get us north of the 5% mark on the 10-Year U.S. Treasury Yield. If we apply the historical median spread between the 10-Year Treasury yield and the Fed Funds rate, that would put us around the 5% mark.

U.S. Equity Momentum to Continue?

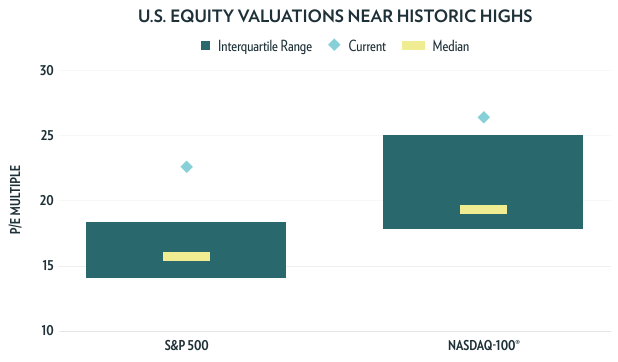

Anecdotally, the biggest concern I’m hearing from advisors as we head into 2025 is the starting valuation on the equity market. And rightly so, as optimism has pushed valuations on the S&P 500 up to the 93rd percentile relative to history. This presents a serious risk should optimism start to sour; however, I don’t think it will. In fact, my 2025 S&P 500 target assumes valuation expansion. Why? I think the buzz around fiscal policy is going to continue, even if pro-growth agenda items are pushed right away. Hopes of tax cuts and regulatory rollbacks could keep the party going.

Source: Bloomberg, Innovator. S&P 500 Index consensus forward 12-month blended PE multiples from 3/31/1990 - 11/26/2024. Nasdaq-100 Index data from 6/29/2001 – 11/26/2024. Interquartile range is the spread between the medians of the upper and lower half of data. Price-to-earnings ratio (“P/E”) is a ratio of a company’s share price to its earnings per share over a year.

Pair sentiment with strong double-digit earnings growth, and that could put us at the 6,700 mark on the S&P 500 Index. The expectation for earnings growth really boils down to an assumption of continued consumer strength and an increase in corporate confidence under the new Trump administration.

Small Caps to Lead the Way?

Small caps have been dominated over the last 11 years, trailing large caps by ~5% per year. I see this trend coming to an end in 2025 for a few reasons. First, relative valuations appear low. This should act as a springboard for a big move if other bullish catalysts play out. Trump 2.0 is very bullish for the asset class, especially given the potential reduction of some burdensome regulations. Pair this with strong growth, and we have a recipe for success.

Some might think this call is counterintuitive with my view on rates staying higher. Not necessarily. As illustrated by the two charts below, small caps appear much more sensitive to economic growth than they are to interest rates. Small-cap correlation to long-term interest rates isn’t clear.

Source: Bloomberg, Innovator. Small Cap 1-Year Returns, represented by the Russell 2000 Index, shown relative to the starting US Federal Funds Rate. Past performance is not necessarily indicative of future results. One cannot invest directly in an index.

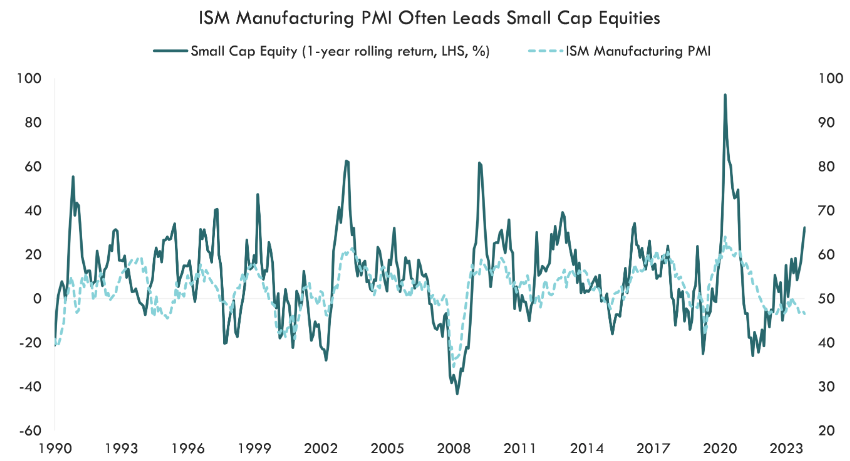

On the flipside, rolling returns have shown correlation with Manufacturing PMIs.

Source: Bloomberg, Innovator. Small-cap equity returns represented by the Russell 2000 Index. U.S. ISM Manufacturing Purchasing Managers Index (“PMI”) Level shown. Monthly data from 12/31/1990 - 10/31/2024. Past performance is not necessarily indicative of future results. One cannot invest directly in an index.

AI Infrastructure May Continue to Dominate

It’s hard for me to imagine a world where AI infrastructure stocks don’t do well in 2025. Entering 2025, AI Infrastructure companies are racing to lead the way in AI. Quite a few of these sector constituents have a backlog of orders, impressive margins, and persistent pricing power. This is not something you see often. In my opinion, it’s a rare opportunity. I know there are many who are concerned about end-user monetization—whether software companies can monetize this AI infrastructure spend—but I think these concerns are overblown and premature. Whether companies can in fact monetize may not matter over the next two to three years. Companies clearly think they can, as indicated by their capital expenditures to date, and I think that spending broadens this year. The Magnificent 7 have already spent half a trillion…

Energy Prices to Abate

New year, new administration. I expect the Biden administration to take elevated energy prices with them. Between reduced regulations and increased production, Trump’s energy agenda could send prices falling fast. What is the administration proposing? An accelerated permitting process for energy projects, increased drilling on public land, removal of burdensome environmental policies, and additional tax incentives for energy producers. All should be positives for energy costs. The big question is, can he get it done?

I believe the answer is yes. This is one area where I think he will have plenty of support in Congress to push ahead.

And there you have my top 5 for ’25.

This material contains the current research and opinions of its author, which are subject to change without notice. This material is not a recommendation to participate in any particular trading strategy and does not constitute an offer or solicitation to purchase any investment product. Unless expressly stated to the contrary, the opinions, interpretations, and findings herein do not necessarily represent the views of Innovator Capital Management, LLC (“Innovator”) or any of its affiliates.

This material is provided for informational purposes only. References to specific securities in this material are provided for informational purposes only and do not constitute a recommendation for any security. Readers should consult with their investment and tax advisers to obtain investment advice and should not rely upon information published by Innovator or any of its affiliates. Past performance does not guarantee future results. The information herein represents an evaluation of market conditions as of the date of publishing, is subject to change, and is not intended to be a forecast of investment outcomes.

This material is provided for informational purposes only and is made available on an “as is” basis, without representation or warranty. The information herein is only current as of the date indicated and may be superseded by subsequent market events or for other reasons. This material represents an evaluation of market conditions as of the date of publishing, is subject to change without notice, and is not intended to be a forecast of investment outcomes. Innovator specifically disclaims all warranties, express or implied, to the full extent permitted by applicable law, regarding the accuracy, completeness, or usefulness of this information, including any forecasts or price targets contained herein, and assumes no liability with respect to the consequences of relying on this information for investment or other purposes.

Past performance is not necessarily indicative of future results. One cannot invest directly into an index. Index performance does not account for fees and expenses.

Certain information herein contains forward-looking statements such as “will,” “may,” “should,” “expect,” “target,” “anticipate,” or other variations of these statements. Forward-looking statements are based upon assumptions which may not occur, while other conditions not taken into account may occur. Actual events or results may differ materially from those contemplated in such forward-looking statements. The forward-looking statements contained herein do not constitute, and should not be relied upon as, investment advice. Such forward-looking statements are not necessarily based upon explicit criteria and assumptions, but rather, represent the opinions of the author. Projections, outlooks, and forecasts do not reflect actual investment results, are not guarantees of future results, and are hypothetical in nature.