May 8, 2023

A Primer on High Yield Bonds

Tom O'Shea, CFA

Director of Investment Strategy

Innovator Capital Management

We believe every asset should serve a purpose and investors should be compensated for the risk they take. When considering adding an asset, it is important to evaluate its impact to the portfolio's expected return, risk, and liquidity. Investors should also consider their time horizon and an asset's tax implications.

High Yield Bonds can Boost a Portfolio's Yield Potential

High yield, or junk bonds are typically issued by early-stage companies or companies with less healthy balance sheets than investment grade issuers. As a result, credit rating agencies deem high-yield issues more likely to default, and thus riskier than Treasuries or investment grade bonds. The enhanced risk forces companies to issue the bonds with higher yields to entice investors to purchase them.

Portfolio managers allocate to high yield bonds for a variety of reasons. The main reason is seeking higher returns and a yield greater than lower-risk fixed income investments.

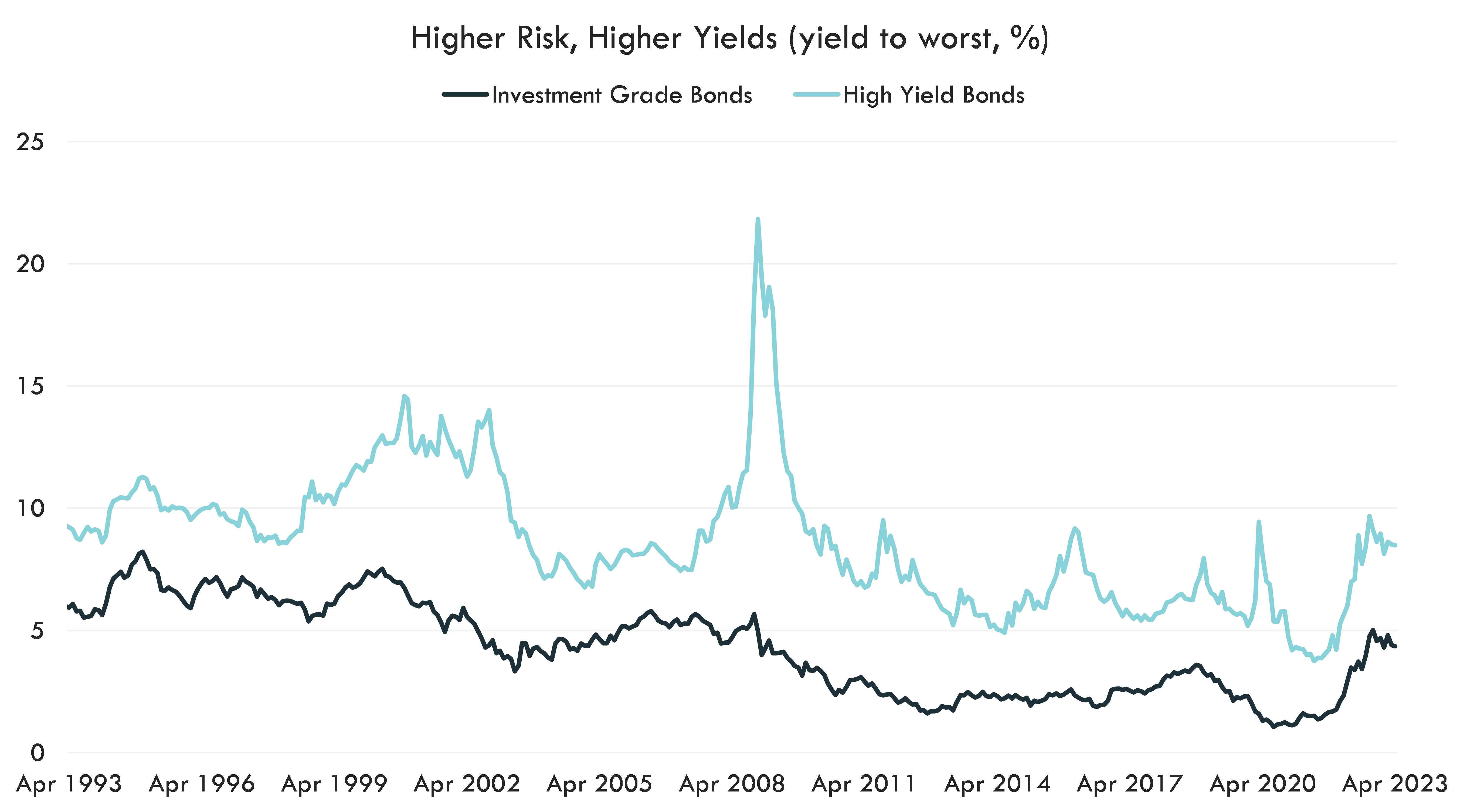

Following the Global Financial Crisis (GFC), investors especially craved yield. The Federal Reserve cut the main policy rate from a peak range of 5%-5.25% down to 0%. As a result, Treasury yields plummeted. The duration-matched Treasury yield moved from 5.12% after the last hike of the pre-GFC tightening cycle to 1.77% following the final cut of the cutting cycle. Prior to the Fed cutting rates, Investment grade investors would have enjoyed a small yield spread of 0.68% over duration matched Treasury holdings. This spread widened to 2.37% once the Fed hit zero. High yield investors experienced yield spreads of 3.46% and 17.66% over their duration-matched Treasury holdings.

Source: Bloomberg L.P., Innovator Research and Investment Strategy. Investment Grade Bonds yield to worst are proxied by Bloomberg U.S. Aggregate bond index. High Yield bonds are proxied by Bloomberg US Corporate High Yield bond index. The yield to worst of a bond is the lowest possible yield that can be received on a bond with an early retirement provision. Monthly data 3/31/1992 - 4/30/2023.

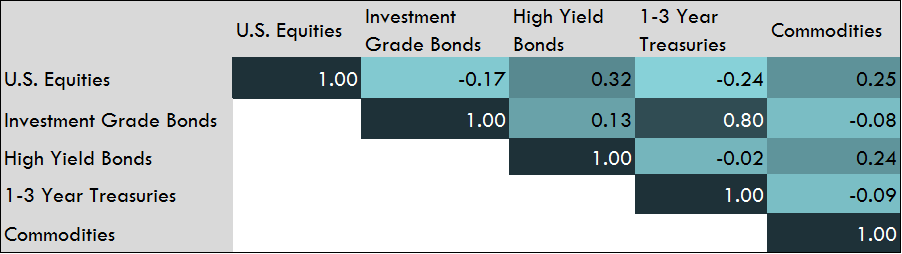

Diversification has also been a major benefit of high yield bonds; they offer low correlations to other major asset classes. In the event of equity market downturns, high yield may not fall quite as low. Similarly, near zero historical correlations to investment grade bonds and short-term Treasuries mean high yield bonds will not necessarily move in the same direction when those asset classes struggle.

Source: Bloomberg L.P., Innovator Research & Investment Strategy. Correlations calculated on daily data from 2/1/1999 - 3/31/2023. U.S. Equities = S&P 500, Investment Grade Bonds = Bloomberg U.S. Aggregate Bond Index, High Yield Bonds = Bloomberg U.S. Corporate High Yield Index, 1-3 Year Treasuries = Bloomberg U.S. Treasury: 1-3 Year Total Return Index, Commodities = Bloomberg Commodity Index.

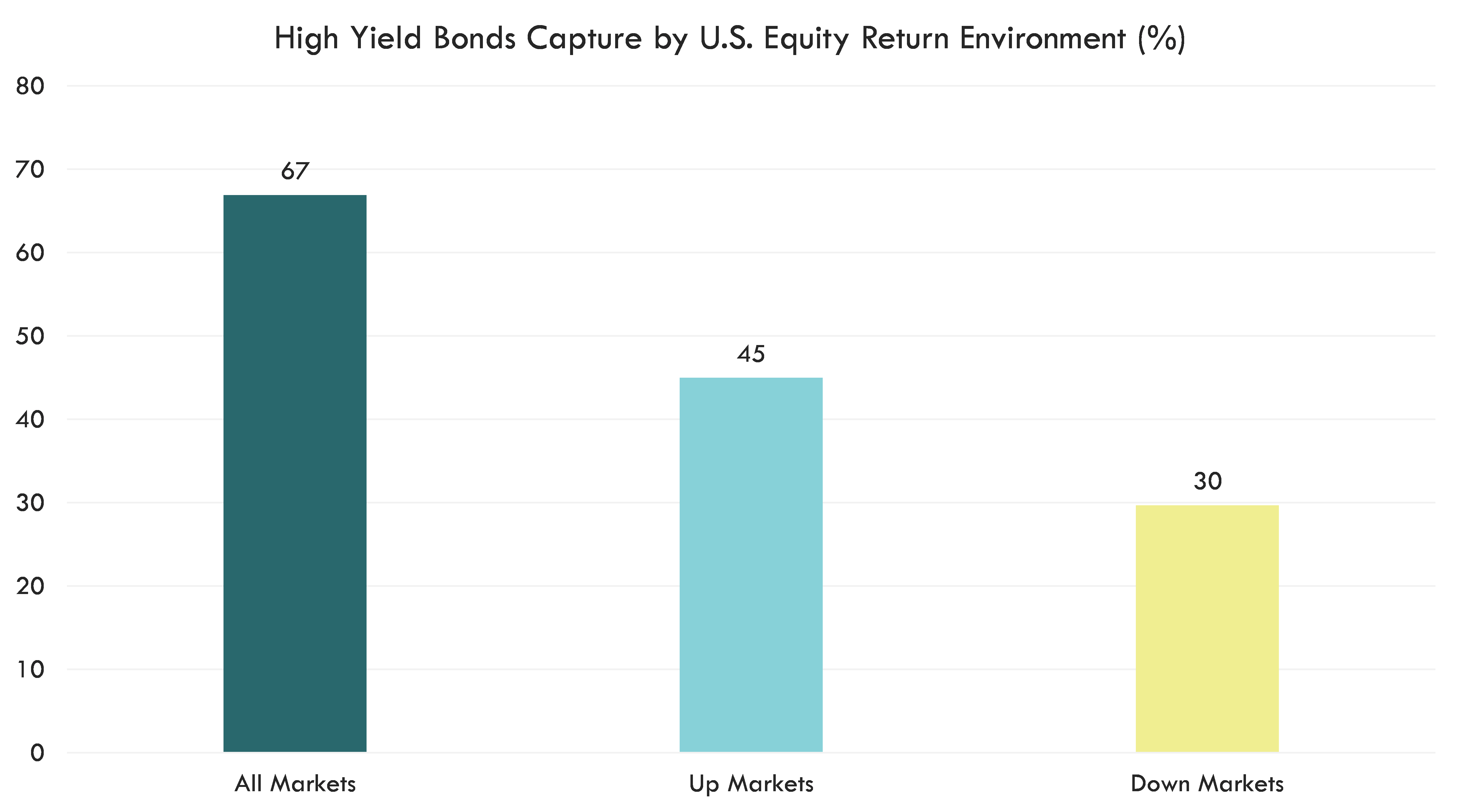

The chart below also demonstrates potential diversification benefits of a high yield bond allocation. In environments when the S&P 500 appreciates for the month, high yield bonds captured 45% of that upside on average. Conversely, negative returning months have resulted in only a 30% average capture of the downside returns. High yield's historically asymmetric payoff profile relative to the S&P 500 may make it an attractive option for investors exploring uncorrelated return opportunities.

Source: Bloomberg L.P., Innovator Research & Investment Strategy. Monthly return data from 3/31/1992 - 4/30/2023. U.S. Equities are measured by the S&P 500 and High Yield bonds are measured by the Bloomberg U.S. High Yield corporate bond index. Past Performance does not guarantee future results.

High Yield has Been Less Sensitive to Rate Movements

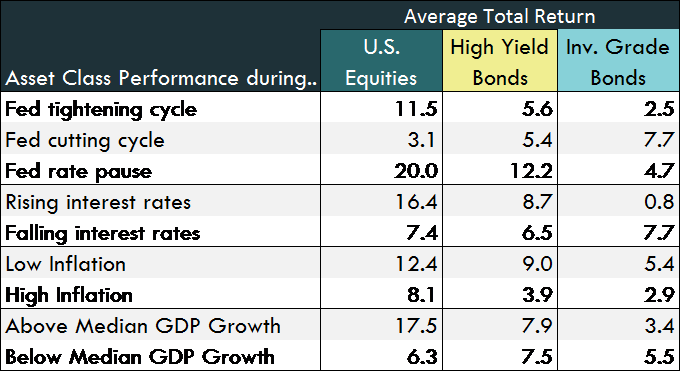

High yield bonds have historically offered less interest rate risk compared to investment grade bonds'; a feature that may be attractive to investors. The Bloomberg U.S. Aggregate Bond index, which serves as a proxy for Investment grade fixed income, has a current duration of 6.5 years. Typically, high yield bonds are issued with maturities below 10 years and offer the flexibility for issuers to call the bond early. Historically, the lower duration (current Bloomberg U.S. High Yield Corporate Bond Index at 4.2 years) has prevented high yield bonds from struggling as much as their investment grade counterparts during rising interest rate environments. High yield bonds have also demonstrated less dispersion during periods of high inflation compared to U.S. equities or the highest quality bonds.

Source: Bloomberg L.P., Innovator Research and Investment Strategy. U.S. equities = S&P 500. High Yield = Bloomberg U.S. Corporate High Yield Bond Index. Investment Grade Bonds = Bloomberg U.S. Aggregate Bond Index. Average Total figures are calculated over 12-month periods from 3/31/1992 – 4/30/2023. Rising/Falling interest rates measured by U.S 10-year Treasury yield. High inflation is headline CPI greater than 3.0% year-over-year. Above median GDP Growth is 4.7%. Past performance does not guarantee future results.

Weak Economic Growth May Weigh on High Yield

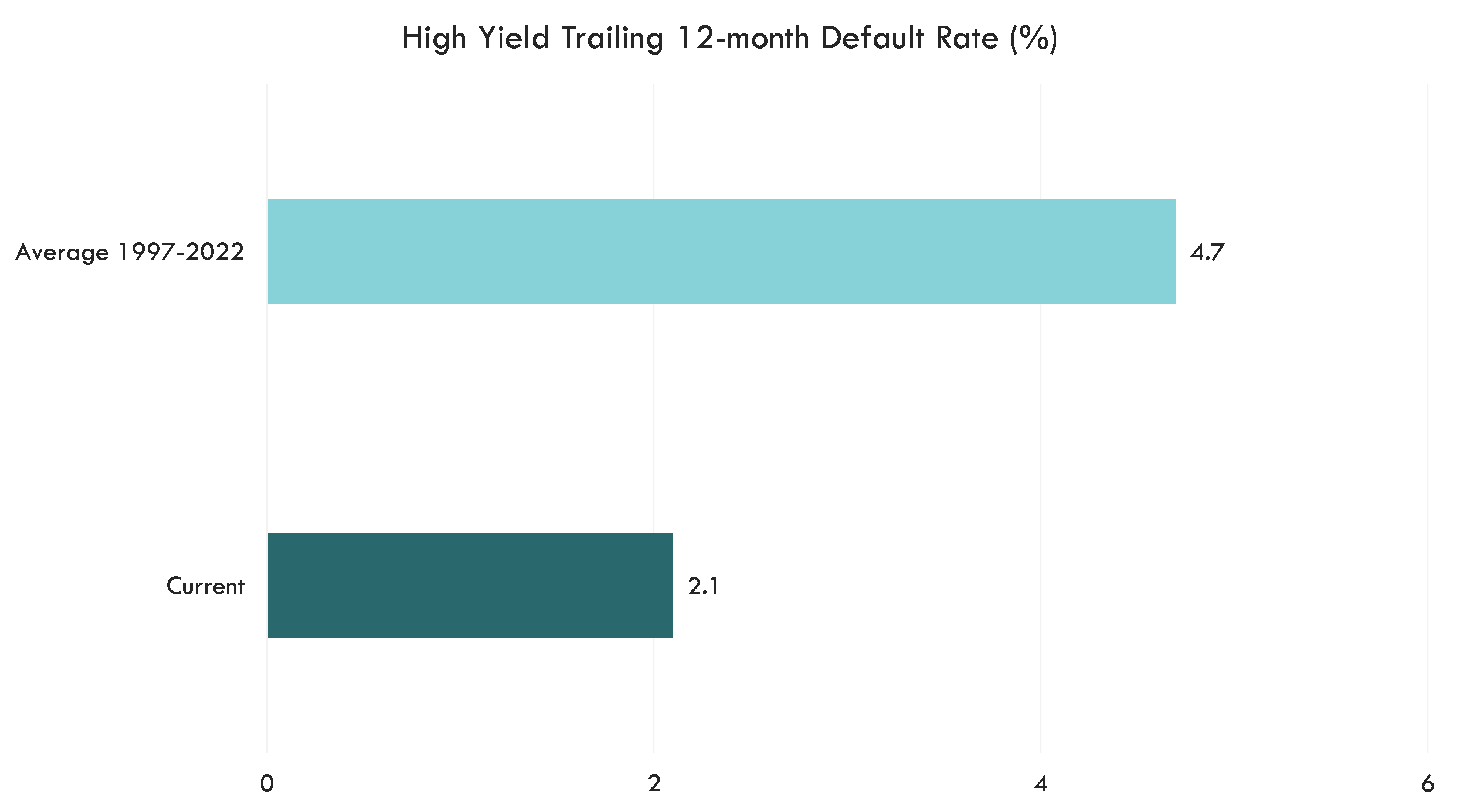

Holding all things constant, high yield bonds are more likely to default than investment grade bonds. Defaults of high yield issuers in the past two years were well below the historic average of 4.7%, with only 27 issuers defaulting. Looking back to 2015-2020, an average of 56 companies per year defaulted on bond issues. Most analysts are expecting default levels to push up toward historical averages over the next 12 months as restrictive monetary policy begins to weigh on corporate earnings. A recession is typically required to drive default rates into a cycle peak.

Source: Bloomberg L.P., Goldman Sachs, Innovator Research & Investment Strategy. Data as of 4/30/2023.

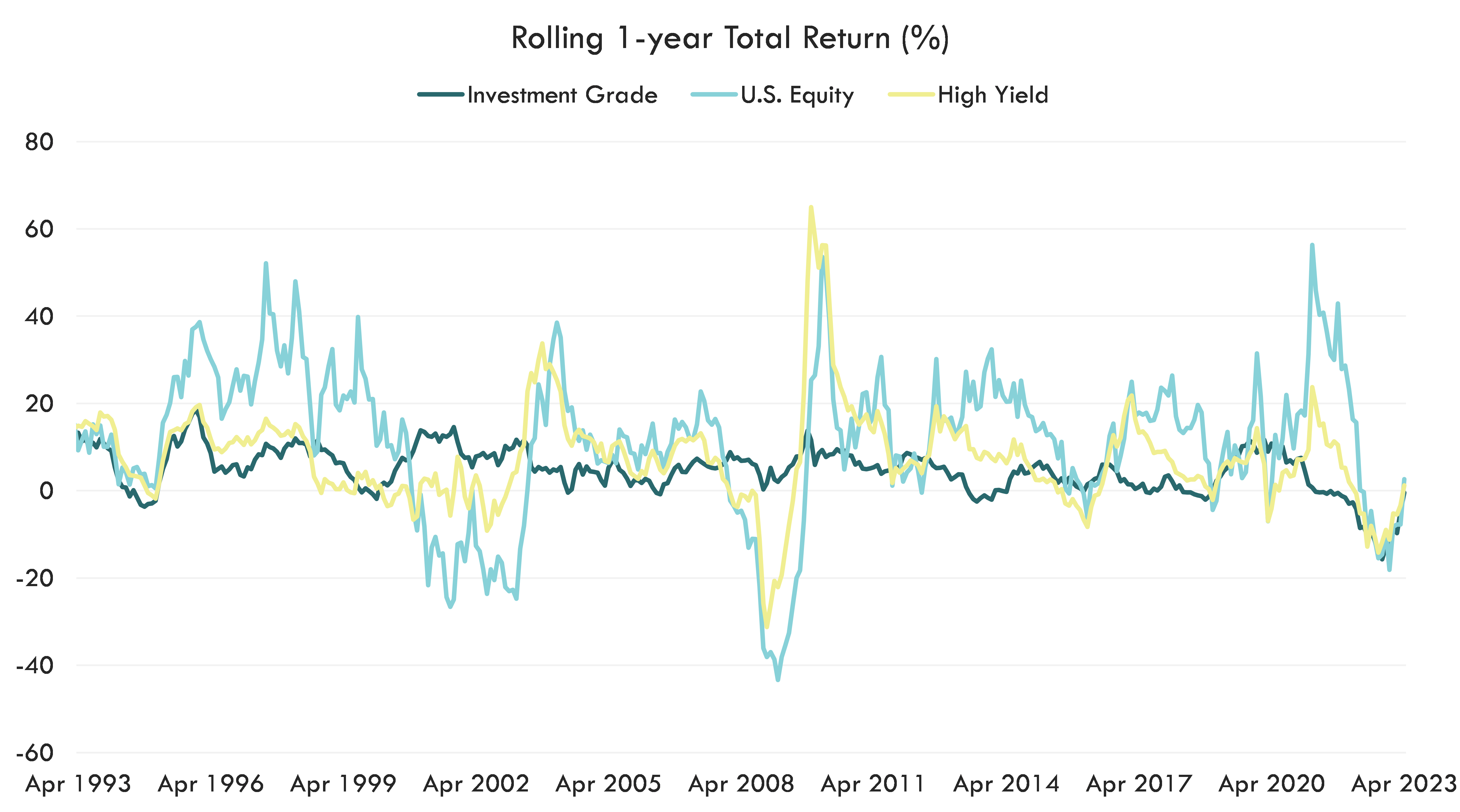

While high yield bonds have a smaller average downside capture ratio compared to U.S. equities, investors can still experience large drawdowns when default rates peak. High yield experienced drawdowns greater than investment grade bonds during the dot-com bubble burst at the turn of the century, the GFC, and the most recent bear market that began in 2022.

Source: Bloomberg L.P., Innovator Research and Investment Strategy. U.S. equity = S&P 500. High Yield = Bloomberg U.S. Corporate High Yield Bond Index. Investment Grade Bonds = Bloomberg U.S. Aggregate Bond Index. Data from 3/31/1992 – 4/30/2023. Past performance does not guarantee future results.

Current Considerations

High yield bonds are often considered valuable additions to portfolios, as they offer high returns per unit of risk. Uncorrelated exposure to high yield has allowed for upside participation and generally smaller drawdowns compared to U.S. equities and investment grade bonds. However, periods of economic distress can lead to correlated returns in the worst possible times. While the S&P 500 dropped to a low of -24.5% in 2022, investment grade and high yield bonds fell 14.5% and 14.8%, respectively.

Many economists are forecasting a recession in the next 12-months. Recession signs are currently flashing in the form of an inverted yield curve and PMIs in contractionary territory. Additionally, higher borrowing costs are beginning to impact corporate earnings. Although high yield bonds are a strategic holding in many portfolios, investors may want to consider other income-generating strategies without the credit exposure to complement their portfolios.

The Bloomberg US Aggregate Bond Index, or the Agg, is a broad base, market capitalization-weighted bond market index representing intermediate term investment grade bonds traded in the United States. The Bloomberg US Treasury: 1-3 Year Index measures US dollar-denominated, fixed-rate, nominal debt issued by the US Treasury with 1-2.999 years to maturity. The Bloomberg Commodity Index is made up of 23 exchange-traded futures on physical commodities, representing 21 commodities which are weighted to account for economic significance and market liquidity. The Bloomberg US High-Yield Corporate Bond Index is a rules-based, market-value-weighted index engineered to measure publicly issued non-investment grade USD fixed-rate, taxable and corporate bonds. The Bloomberg US Corporate High Yield Bond Index measures the USD-denominated, high yield, fixed-rate corporate bond market. The S&P 500 is a stock market index tracking the stock performance of 500 of the largest companies listed on stock exchanges in the United States.

Credit ratings: Standard & Poor's and Moody's study the financial condition of an entity to ascertain its creditworthiness. The credit ratings reflect the rating

agency's opinion of the holdings' financial condition and histories. The ratings displayed are based on the highest of each portfolio constituent as currently

rated by Standard & Poor's and Moody's. Long-term ratings are generally measured on a scale ranging from AAA (highest) to D (lowest), while short-term

ratings are generally measured on a scale ranging from A-1 to C.

Correlation, in the finance and investment industries, is a statistic that measures the degree to which two securities move in relation to each other. A positive correlation indicates the securities move in line with each other while a negative correlation indicate the opposite.

High-yield bonds, or junk bonds, are bonds that pay higher interest rates because they have lower credit ratings than investment-grade bonds. High-yield bonds are more likely to default, so they pay a higher yield than investment-grade bonds to compensate investors.

Investment-grade bonds are higher rated bonds, typically seen as safer and more stable investments that are tied to corporations or government entities that have a positive outlook. Investment-grade bonds contain “AAA” to “BBB-“ (or Aaa to Baa3 for Moody's rating scale) ratings and will usually see bond yields increase as ratings decrease.

The Global Financial Crisis, or GFC, refers to the period of extreme stress in global financial markets and banking systems between mid 2007 and early 2009.

The Consumer Price Index (CPI) is a measure of the average change over time in the prices paid by urban consumers for a market basket of consumer goods and services.