March 3, 2025

Tariffs, DOGE, and Your Portfolio:

The Net Impact of Trump 2.0

Tim Urbanowicz, CFA

Head of Research & Investment Strategy

Innovator Capital Management

We're just over a month into Trump's second presidential term, and so much has already transpired. From spending cuts to tariffs and regulatory easing, investors are left trying to piece together what it all means. Over the past month, I have been on the road meeting with advisers, and the number one question I hear is, “With so many different policies and proposals floating around, what is the net impact for investors?”

In this blog, I break down three of the most impactful proposals from the Trump administration, assess their implications, and explain why I believe, on balance, these policies will be positive for U.S. equity investors.

Elon Musk and DOGE

The Department of Government Efficiency, led by Elon Musk, has dominated headlines since Inauguration Day, aggressively pursuing headcount and spending cuts. While I am highly skeptical that they'll achieve the full $2 trillion in cuts they have advertised, there are real signs of progress. Some argue these reductions will negatively impact the economy and markets—I disagree.

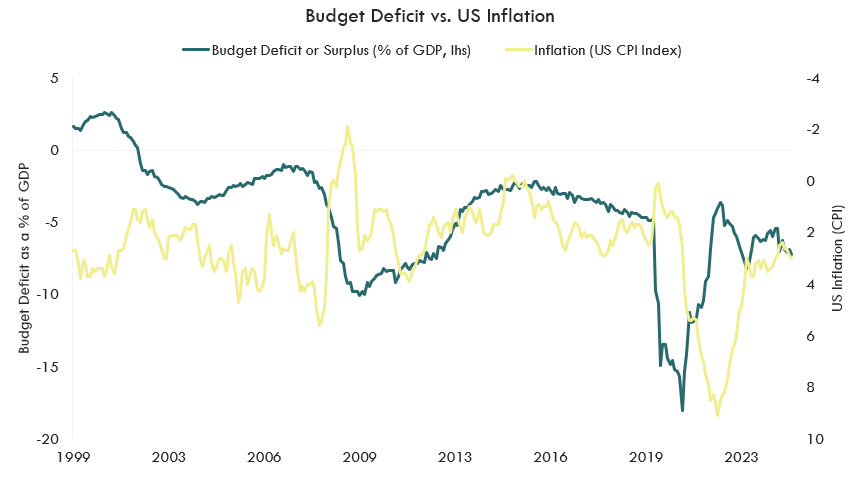

Excessive government spending fuels inflation. The past four years provided a textbook example, with rampant spending resulting in the deficit averaging ~6% of GDP since 2022. Even though inflation has come down from its peak, it remains sticky and deeply embedded in the economy. One major factor? The $1.83 trillion deficit in 2024¹.

Source: Bloomberg, Innovator. LHS = U.S. Budget Deficit (-) or Surplus (+) as a percentage of GDP. RHS = U.S. CPI 12-month percentage change. Data from 12/31/1999 - 1/31/2025.

If DOGE is successful—and that is a big if—I would have more confidence that inflation and bond yields will decline. It will not happen overnight, but meaningful spending cuts would be a step in the right direction. In my view, the recent dip in bond yields suggests the market is already pricing in some level of fiscal restraint.

I understand that mass government layoffs sound like a short-term economic hit, but with the labor market still strong, my view is that displaced workers will likely transition into the private sector, ultimately making the economy more productive through more efficient labor allocation.

Many fiscally conservative Republicans in Congress will not support extending the 2017 tax cuts if it means ballooning the deficit. However, spending cuts increase the odds that tax reform could actually happen. If DOGE can identify meaningful savings, a more feasible path for tax cuts will open.

The Shifting Regulatory Landscape

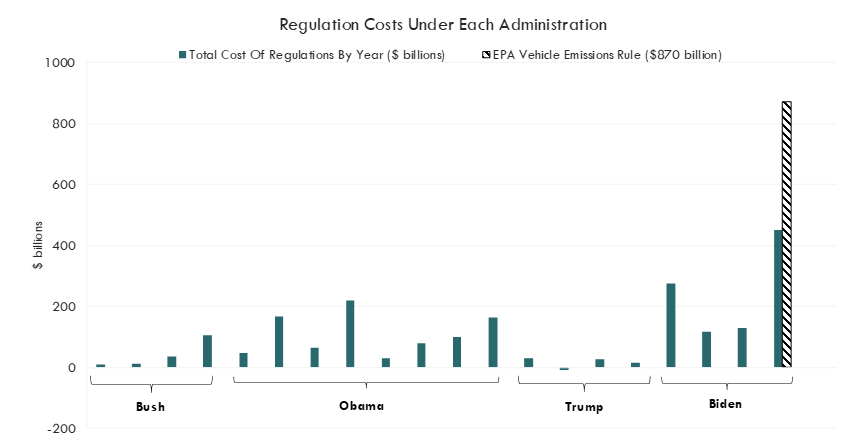

On the regulatory front, we seem to be moving from one extreme to another. As shown in the chart below, the Biden administration imposed the highest regulatory costs of any modern presidency—by a wide margin. These regulatory costs hit companies across the board but disproportionately burdened smaller businesses that lack the resources to absorb them. By contrast, during Trump's first term, regulatory costs were the lowest in recent history.

Sources: Piper Sandler and American Action Forum, The Biden Regulatory Record. https://tinyurl.com/z7a8tna8 [Retrieved 3/4/2025]. Bush Administration Dates = 1/20/2001 – 1/20/2009. Obama Administration Dates = 1/20/2009 – 1/20/2017. Trump Administration Dates = 1/20/2017 – 1/20/2021. Biden Administration Dates = 1/20/2021 – 1/20/2025.

This shift helps explain why small business optimism has ticked up since the November election. Lower regulatory costs should provide a tailwind for U.S. equities broadly, with sectors like financials and energy set to benefit the most after bearing the brunt of regulatory costs over the past four years.

Tariffs: The Wildcard

Tariffs are a major source of uncertainty, and visibility into their full impact remains low. Depending on how things unfold, they could have either a minimal or significant economic effect, but they will undoubtedly be a continued source of market volatility. Estimates vary, but some projections suggest a full-scale tariff regime could shave around 1% off of GDP².

Many view tariffs as inflationary. In my view, they act more like a tax on consumers—a one-time cost increase. Given the price pressures of recent years, additional costs from tariffs could be the tipping point for many, particularly lower-income consumers who are already struggling.

In the short term, that is a negative. Investors would get spooked, recession fears may resurface, earnings growth could slow, and volatility will likely persist. In the medium to long term, the effects may not be entirely negative. Inflation remains sticky and consumer spending makes it difficult to rein in. Tariff-driven demand destruction—while painful in the short run—could ultimately help curb price pressures. Everyone wants inflation to come down with no economic pain. While I hope it does, that is not how it typically works.

The Bottom Line

Policy uncertainty is likely to drive continued volatility, especially given the sheer volume of moving pieces. But net-net, I believe Trump 2.0 will be a tailwind for U.S. equities. Tariffs are a risk, depending on their implementation, but spending cuts and regulatory rollbacks could help drive inflation lower and create a more efficient economy—both long-term positives for investors.

1. Source: Fiscal Data, U.S. Department of the Treasury. https://tinyurl.com/4743pnc2 [Retrieved 3/6/2025]. The deficit shown is that of the 2024 Fiscal Year (10/1/2023 – 9/30/2024).

2. Source: The Budget Lab, Yale University, “The Fiscal, Economic, and Distributional Effects of 20% Tariffs on China and 25% Tariffs on Canada and Mexico”. https://tinyurl.com/2nwjtfw5 [Retrieved 3/6/2025]. 2024 deficit in connection with the 2024 Fiscal Year. The Budget Lab projects a 0.64% decrease in Real GDP growth during 2025 arising out of the Economic and Fiscal Effects of China, Mexico, and Canada Tariffs.

This material contains the current research and opinions of its author, which are subject to change without notice. This material is not a recommendation to participate in any particular trading strategy and does not constitute an offer or solicitation to purchase any investment product. Unless expressly stated to the contrary, the opinions, interpretations, and findings herein do not necessarily represent the views of Innovator Capital Management, LLC (“Innovator”) or any of its affiliates.

This material is provided for informational purposes only. References to specific securities in this material are provided for informational purposes only and do not constitute a recommendation for any security. Readers should consult with their investment and tax advisers to obtain investment advice and should not rely upon information published by Innovator or any of its affiliates. Past performance does not guarantee future results. The information herein represents an evaluation of market conditions as of the date of publishing, is subject to change, and is not intended to be a forecast of investment outcomes.

This material is provided for informational purposes only and is made available on an “as is” basis, without representation or warranty. The information herein is only current as of the date indicated and may be superseded by subsequent market events or for other reasons. This material represents an evaluation of market conditions as of the date of publishing, is subject to change without notice, and is not intended to be a forecast of investment outcomes. Innovator specifically disclaims all warranties, express or implied, to the full extent permitted by applicable law, regarding the accuracy, completeness, or usefulness of this information, including any forecasts or price targets contained herein, and assumes no liability with respect to the consequences of relying on this information for investment or other purposes.

Investing involves risk. Principal loss is possible. Past performance is not necessarily indicative of future results. One cannot invest directly into an index. Index performance does not account for fees and expenses.

Certain information herein contains forward-looking statements such as “will,” “may,” “should,” “expect,” “target,” “anticipate,” or other variations of these statements. Forward-looking statements are based upon assumptions which may not occur, while other conditions not taken into account may occur. Actual events or results may differ materially from those contemplated in such forward-looking statements. The forward-looking statements contained herein do not constitute, and should not be relied upon as, investment advice. Such forward-looking statements are not necessarily based upon explicit criteria and assumptions, but rather, represent the opinions of the author. Projections, outlooks, and forecasts do not reflect actual investment results, are not guarantees of future results, and are hypothetical in nature.