August 28, 2023

The Soft Landing Consensus

Tim Urbanowicz, CFA

Head of Research & Investment Strategy

Innovator Capital Management

A string of CPI readings heading in the right direction…. a labor market and consumer that are still intact. All of the sudden, the recession consensus has given way to a soft landing. Should this be surprising though? If you look back historically, it shouldn’t be. In fact, in each of the past six recessions (ex-COVID), as the Fed rate hike cycle reached its conclusion, consensus leaned towards a soft landing…even in 2007.

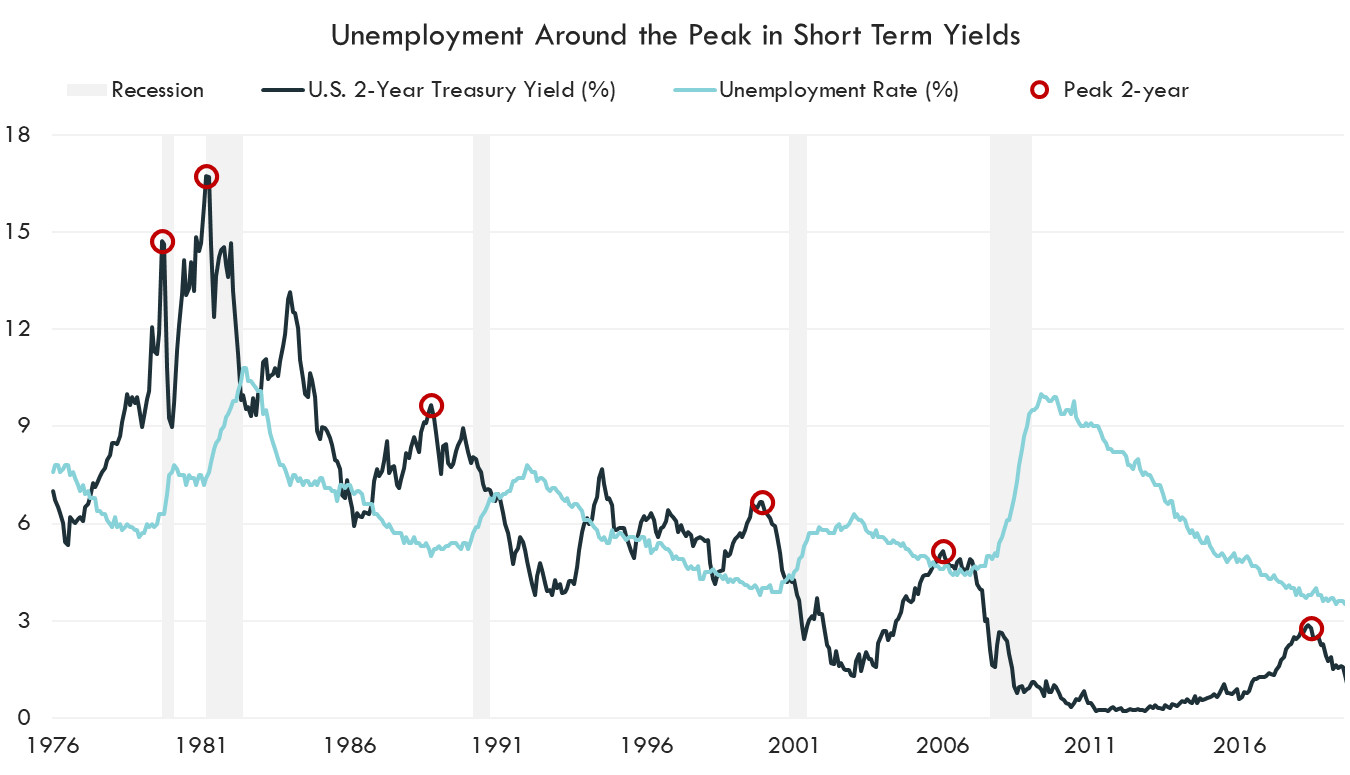

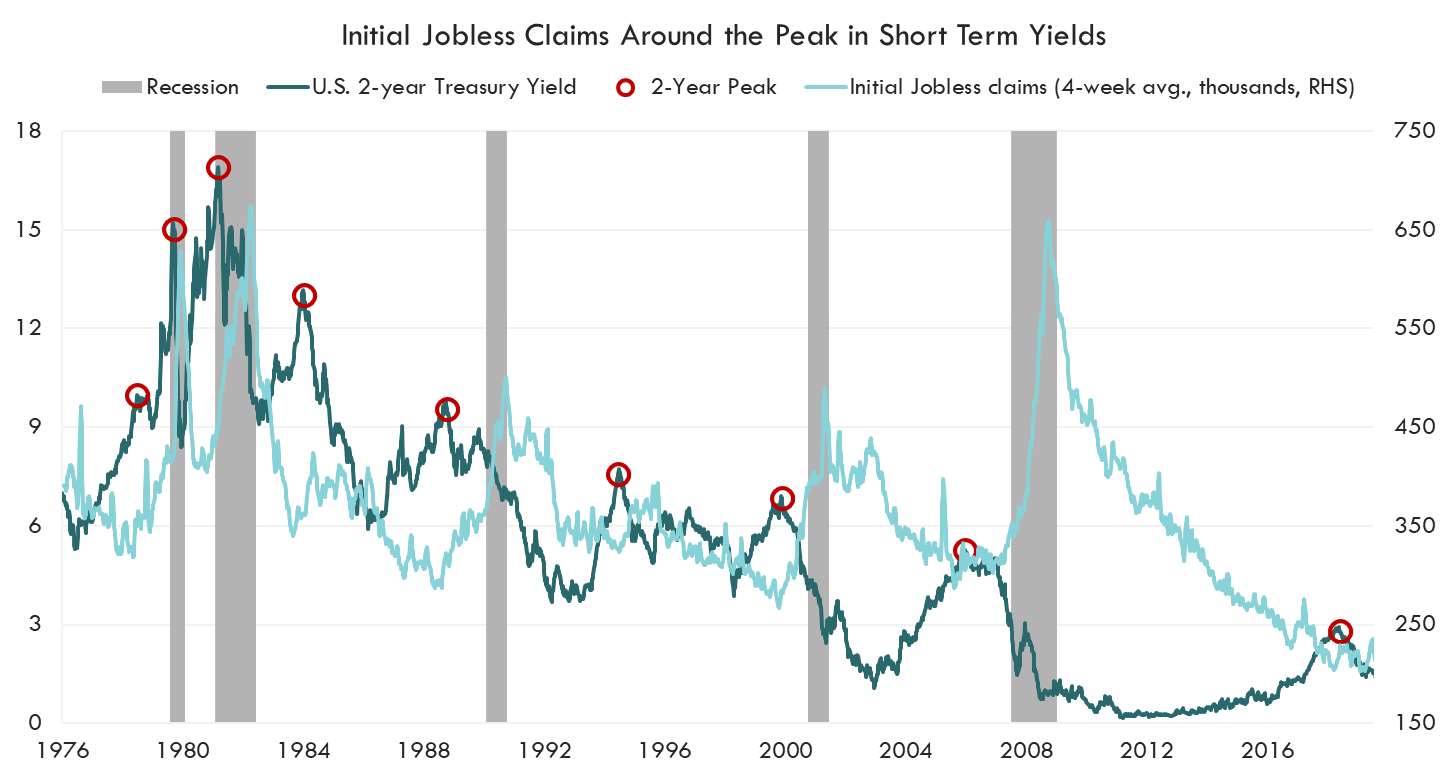

Why is this the case? In most instances, the pause is signaled before any major damage starts to show up in the labor market. As shown in the charts below, initial claims and unemployment both begin to rise, on average, within 2.5 months of the peak in short term yields†. Inflation is falling, the Fed’s work is nearly done, and the labor market appears to be on solid ground, but that doesn’t mean the soft landing is necessarily going to play out. In the majority of cases historically, it hasn't.

Source: Bloomberg LP, US Unemployment, US Generic 2 Year Treasury Yield, 1976-2016

Source: Bloomberg LP, Initial Jobless Claims, US Generic 2 Year Treasury Yield, 1976-2016

Will the soft landing be delivered this time around? Potentially, but over the past year, we have consistently highlighted the sting of monetary policy is always felt with a delay. It’s important not to be fooled into thinking it’s a done deal because the labor market has held up so well to this point.

Hard Landing or Soft Landing, Pauses are Generally Profitable for a Time

Market timing is never a good idea, but it can be particularly damaging as the hike cycle winds down. Sitting on the sidelines and waiting for an event that may or may not even happen can be costly, even in the event of a hard landing.

Investors always get excited around the prospect of a Fed pause, and rightly so. Inflation has been the focal point – it’s the topic that moves markets up and down. Once the Fed gets inflation under control, markets typically rally. The charts below highlight this dynamic, showing the rally in equities as each of the last 7 hike cycles came to a close. Hard landing or soft landing, there is a period after short-term yields peak when equities run…and in some instances, run for a while.

Source: Bloomberg LP, Innovator Research & Investment Strategy, S&P 500 Index, Data from 1980-2023. Periods shown represent the returns following the peak in the 2Y treasury. Past performance is not indicative of future results.

In the case of the hard landings, once investors figure out the issue is no longer inflation -- but instead job loss and economic pain -- the rally quickly transitions to a sell-off. Regardless, missing the pause/pivot rally is not optimal, and highlights the importance of cautiously remaining invested.

Is the Rate Peak Rally Behind Us?

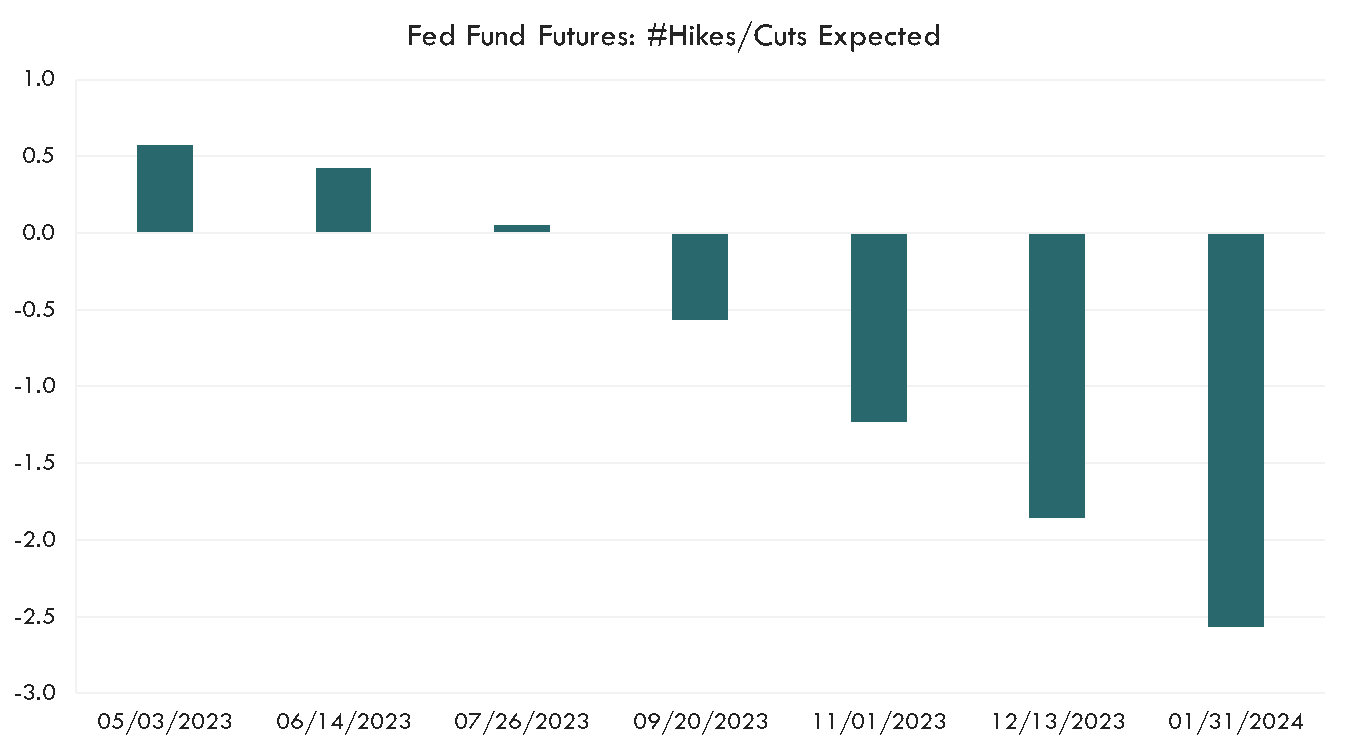

Coming into 2023, the market had high hopes that the rate hike cycle was over. At one point, Fed fund futures were pricing in multiple cuts through the end of December, and as of the time of writing, the 2-year yield peak of 5.07 has yet to be topped (although we are currently within 4bps). These hopes for lower rates helped spur the best start to the year since 1997. So that begs the question, is the rate peak rally behind us?

Source: Bloomberg LP, Fed Fund Futures, 3/31/2023-1/31/2024

While there will likely still be excitement when the hike cycle comes to an end, any upside may be constrained given the run up we’ve already seen in the equity market this year. Equity valuations have been taken back to early 2022 levels and are well above the long-term average, leaving less room for good news to drive outsized returns.

When it comes to the portfolio, it’s important to continue to focus on being risk aware, and not risk off. Keeping clients invested is not always easy, but has been important around the peak in short term yields historically.

†The 2-year treasury gives a good view into market expectations for the Fed.

The Consumer Price Index, or CPI, measures the overall change in consumer prices based on a representative basket of goods and services over time.