July 3, 2023

Timing is Everything

Tim Urbanowicz, CFA

Head of Research & Investment Strategy

Innovator Capital Management

Timing is everything. In baseball, it can be the difference between a foul ball and a home run. In golf, it can be the difference between a drive down the middle of the fairway and a snap hook left, or push right, out of bounds. And at the airport TSA checkpoint, it can be the difference between a random screening and getting through smoothly. When it comes to financial markets…timing is very hard to get right.

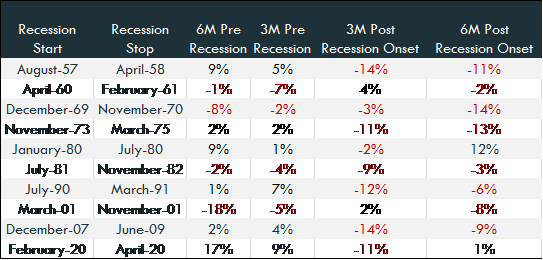

The recession debate seems to have been raging on for well over a year now. For investors, perhaps as important as the debate itself, is the timing. As shown in the table below, historically, in the 3- and 6-months leading up to a recession, U.S. equities have produced a positive total return 60% of the time. On the contrary, once the recession begins, the 3- to 6-months post-onset, equity returns have been negative 80% of the time.

Source: Bloomberg LP, S&P 500 Index, Innovator Research & Investment Strategy, as of 5/31/2023. Past performance is not indicative of future results.

History aside, this time around, the timing conversation is more important than it has ever been. In this month’s newsletter, we dive into why timing is so important, where various economies across the globe stand, and what it all means for investment portfolios.

What a Difference a Year Makes

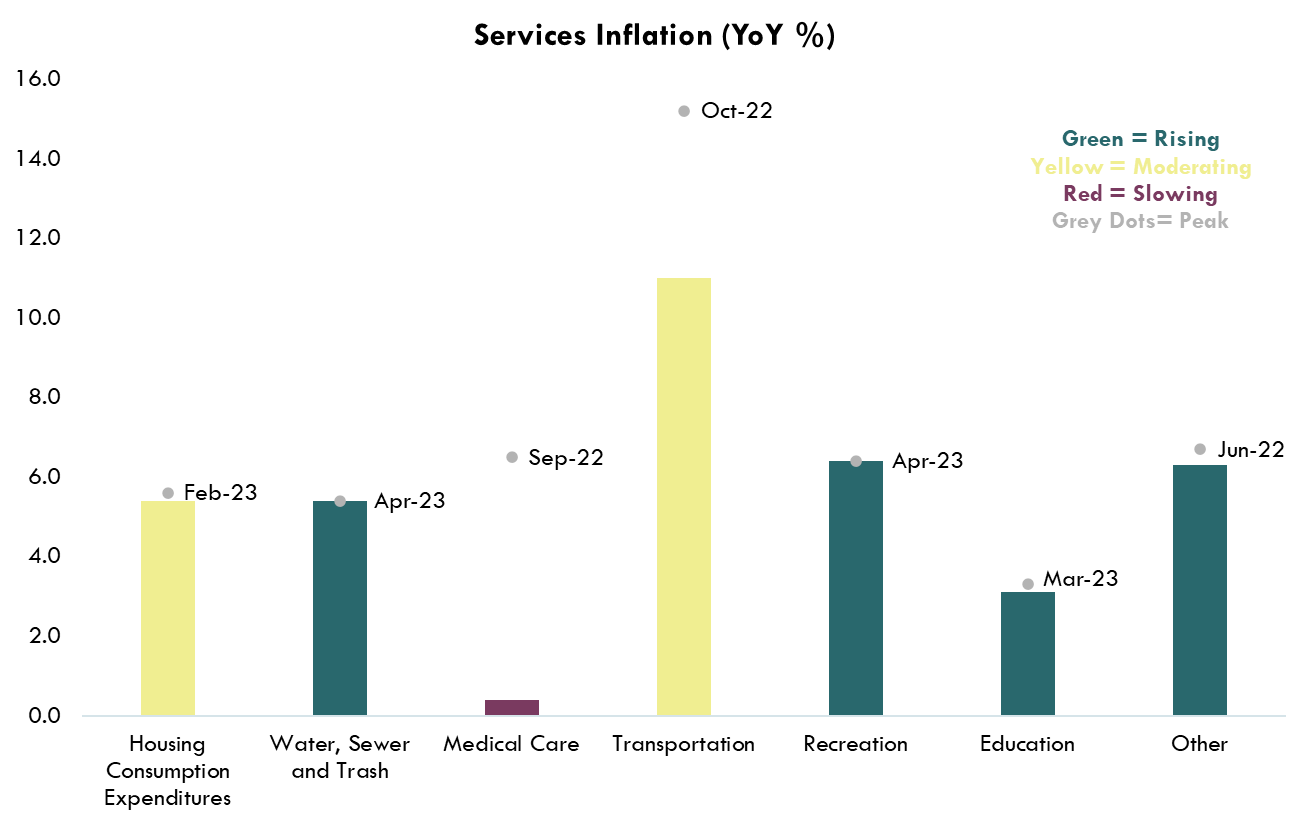

While headline CPI has fallen significantly in the U.S., down to a 4% year over year increase since the June 2022 high of 9.1%, investors need to remember that core inflation has barely budged. From the September 2022 high, core has moved down just 1.3%, from 6.6% to 5.3%. While the lag of the shelter component is playing a big role, several other components within services have shown little to no progress (see chart below).

Source: Bloomberg LP, as of 6/28/2023, US Core CPI, Innovator Research & Investment Strategy

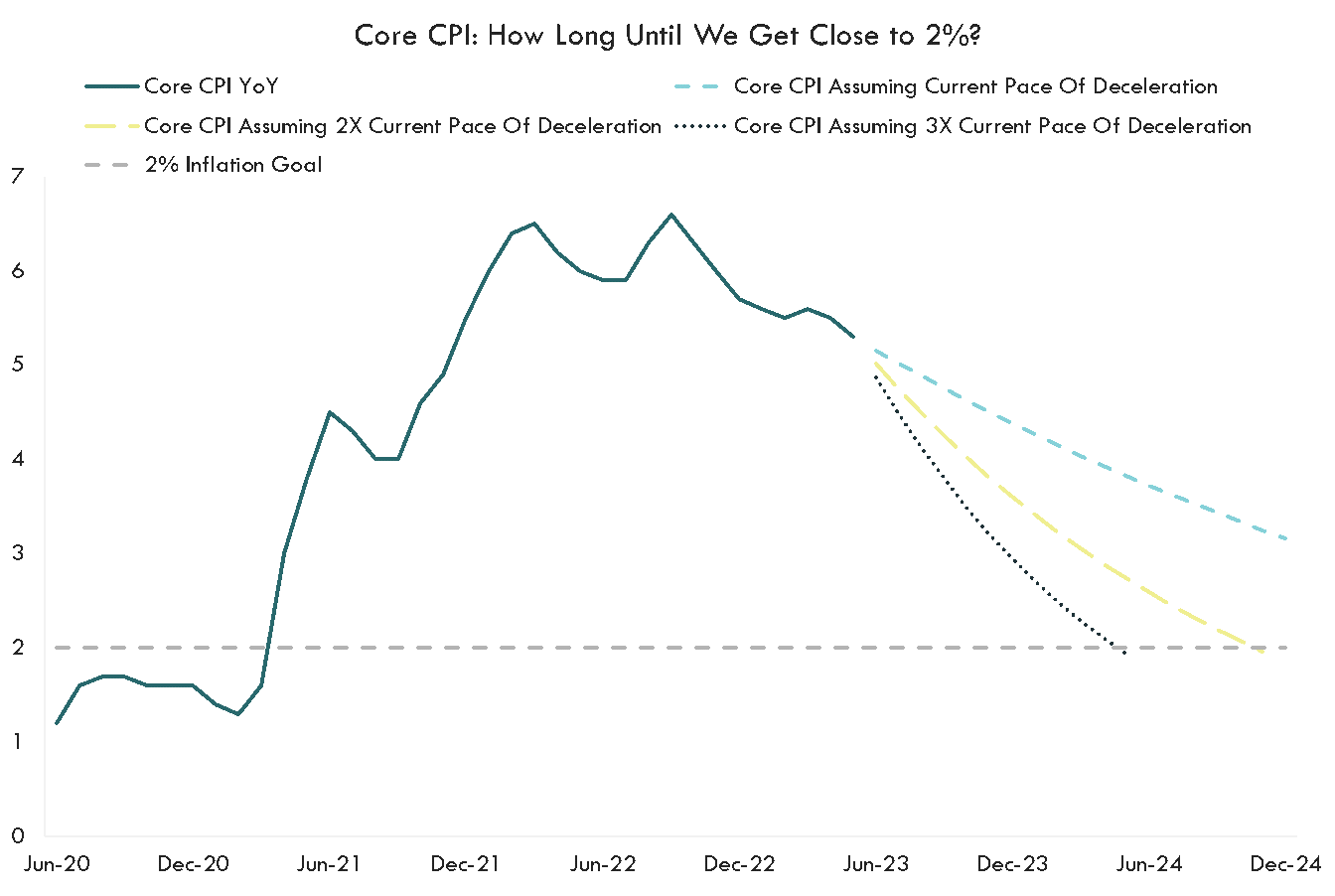

How long will core take to get down near the 2% target? The chart below looks at the path core CPI has taken since the initial spike in late 2020. It also shows the trajectory if the current pace of disinflation since the September peak, were to continue, double, or triple. Even a drop of 8% per month, 3X the pace we have seen up to this point, would leave core well above the 2% target by the end of the year.

Source: Bloomberg LP, Innovator Research & Investment Strategy, US Core CPI, 1/2022-6/2023

In my view, this is what makes the timing of a potential recession equally as important as the recession itself. A recession in late 2023 would look a lot different than a recession in late 2024. Core inflation is likely to remain well above target for the remainder of 2023, and this handcuffs the Fed’s ability to step in to cushion the blow from a 2023 recession. Jumping in to save a falling economy too early, risks eroding the progress that has been up to this point.

Late next year, however, this may not be the case. As core inflation has more time to fall, the Fed toolbox has a better chance of opening up and softening the recessionary blow. The hesitation at 2.5%-3% looks a lot different than the hesitation at 4%-4.5%.

What About Other Developed Market Economies?

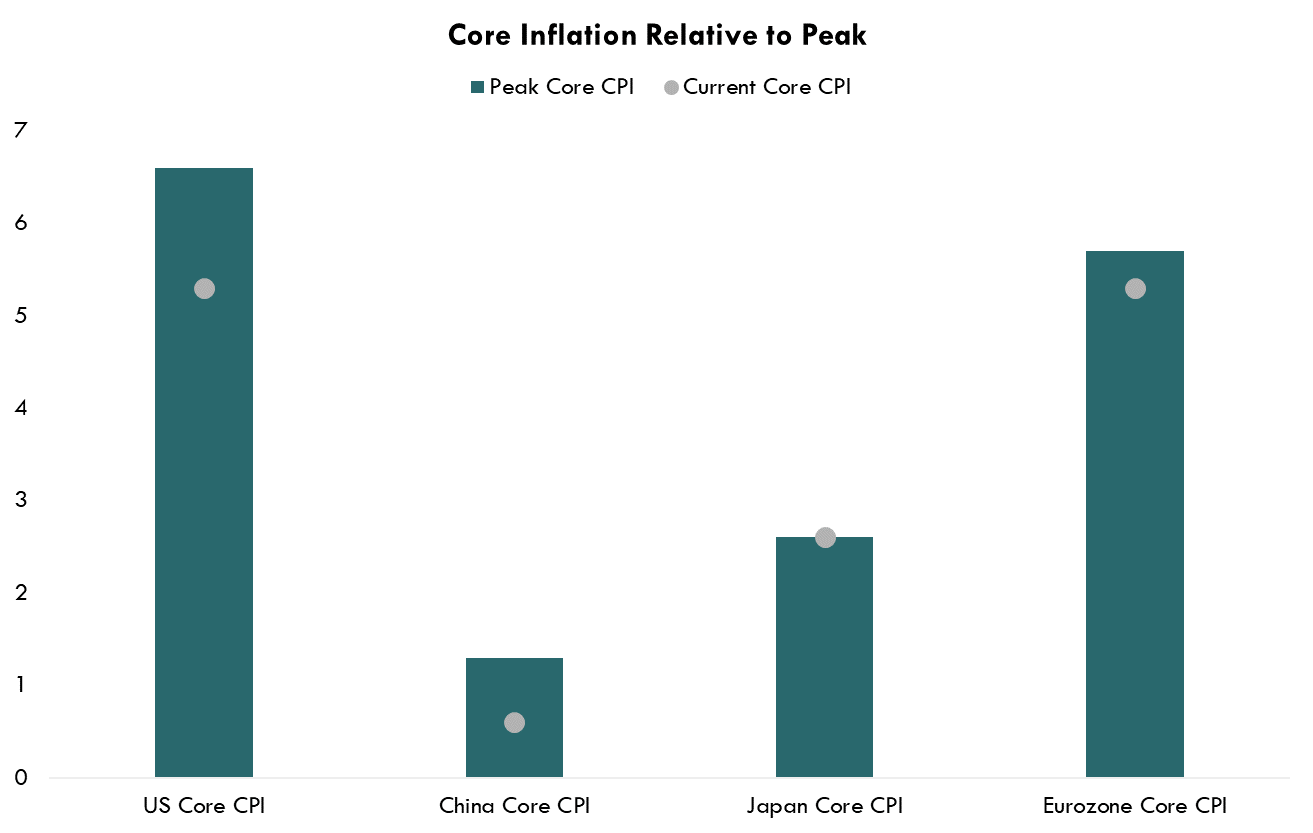

What about other developed market economies? The chart below looks at the most recent core inflation print across other developed market economies, relative to peak.

Source: Bloomberg LP, US, China, Japan, Eurozone Core CPI as of 6/28/2023

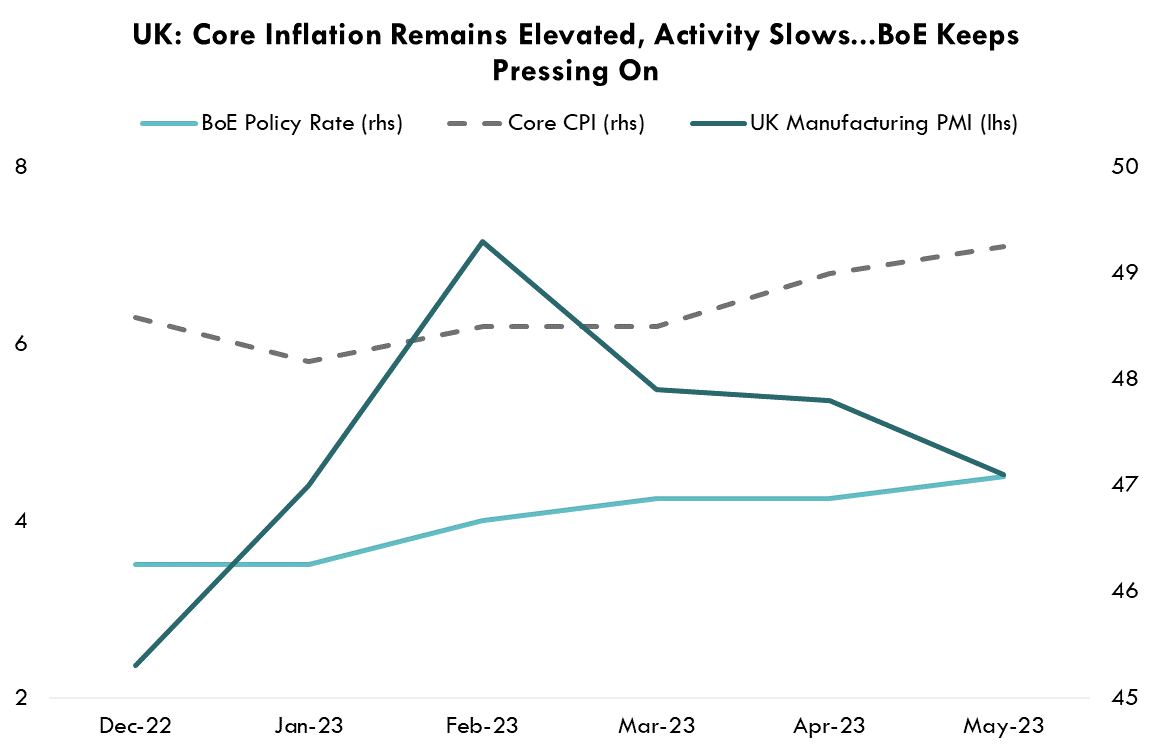

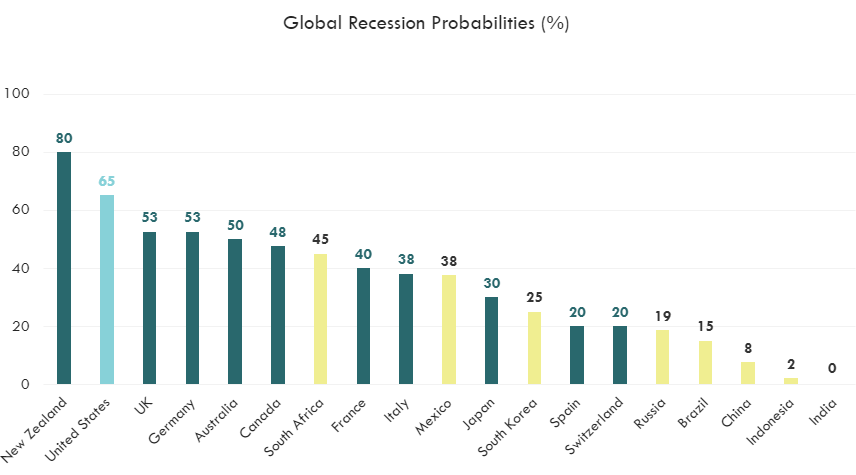

Economies such as the UK, where activity is already showing signs of rolling over and inflation continues to march higher, are especially vulnerable. In the case of the UK, the BoE is still raising rates aggressively, and is unlikely going to be able to transition to rate cuts until more progress is made. This comes at a time where the probability of a near-term recession sits at the highest level relative to all other developed market economies across the globe.

Source: Bloomberg LP, S&P Global/CIPS UK Manufacturing PMI, Core CPI, BoE Policy Rate, 12/2022-5/2023

Europe appears a little better off. Technically, while in a recession, the disinflation process is well underway, and the ECB is likely nearing the end of its rate hike campaign. Japan appears among the best positioned, with growth remaining strong and inflation at contained.

Source: Bloomberg LP, 6/30/2023, Global Recession Probabilities

For the Portfolio

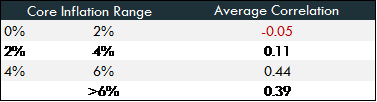

For investment portfolios, the difference in timing could be night and day. In addition to the potential difference in drawdowns across global equity markets, it’s also questionable how much value fixed income will provide throughout a drawdown, especially if the Fed keeps rates elevated. Will the diversification benefits that investors rely on when equities are falling come through? In my view, there is a much better chance once core inflation has time to cool further. As shown in the table below, historically, the higher core CPI has been, the higher the correlation between equities and bonds. Said another way, higher core inflation means less value from a bond allocation.

Source: Bloomberg LP, US Core CPI, Bloomberg US Aggregate Bond Index, S&P 500 Index, Data from 1/1979-5/2023

The good news for investors is that as time goes on, a 2023 U.S. recession looks less and less likely. Our view has always been that 2023 was likely pre-mature. Don’t get me wrong, cracks are starting to form (read: The Storm Clouds are Getting Closer blog for more), but those cracks are going to take time to materialize. We continue to be advocates for keeping a risk-aware stance while keeping clients invested and diversified across the global equity market.

As shown in the opening table, recession worries haven’t necessarily meant negative equity markets before the storm actually hits. Given the uncertainty of a recession at all, going risk off could be a costly mistake. This is a lesson many who went to cash at the start of the year have learned the hard way.

The Consumer Price Index, or CPI, measures the overall change in consumer prices based on a representative basket of goods and services over time.

BoE: Bank of England

ECB: European Central Bank